A question impact investors often face is “Why Impact?” or, in another phrasing, “Won’t the money find its way to the opportunities anyway?” Committed believers in capitalism tend to be committed to the notion that capital will, like water, always find its level — risk will be priced by market participants, and the system should otherwise be left to its own devices. What, then, is the point of adding the complication of impact measurement? Should capitalists who don’t care about non-financial outcomes pay attention to the development of the impact space anyway?

Various market participants have come up with different responses to this, and they tend to have a few things in common. A key point is that impact investments facilitate good ESG practices.

Here’s a list:

What You Look For Is What You See. Looking at the world with an impact lens will push investors to seek out certain types of opportunities more than others. This might narrow the investable opportunity set perhaps. But it will also screen out deals earlier that might otherwise take up a deal team’s time. The net effect is that companies and technologies and ideas will get funds and attention that would otherwise languish.

Societal attitudes are changing. This has implications for both capital-raising and for the investment opportunity set.

On the capital raising side, individual investors are allocating more and more to impact strategies of different kinds. Morgan Stanley launched its Investing with Impact Platform for its retail investor and high-net-worth (HNW) clients in September 2012. In November 2013, it committed to raising $10bn on the platform in 5 years, and by November 2018 it had raised $25bn. In September 2019, Barron’s noted that UBS had invested $225m in KKR’s first Global Impact fund. A broader measure is the capital in “sustainable investing” strategies in general — of which impact is a subset. The Global Sustainable Investment Alliance published its fourth biennial report in 2018, and noted AUM in the space had grown to $30tn, up from $22tn in 2012.

Investment opportunities are shifting in favor of impact investors too. Concerns around the environmental costs of raising cattle made Beyond Meat, and its rival Impossible Foods, possible. Global sales of fair trade products grew by 8% in 2018, and topped $9bn for the first time.

Preparing for the future. Impact investing is distinct from ESG, but the two have much in common. ESG-aware ownership of company might align with a statement such as “We want to behave responsibly” and seek to install LED lighting in company facilities even when cost savings might be modest. An impact investor attempts to address a problem more specifically, and might then set about investing in the LED company itself. Some observers have suggested “how you own” your company expresses your ESG orientation, and “what you own” expresses your impact investing credentials.

ESG has become increasingly mainstream, illustrated by several reports of changing attitudes among investment managers. At the MSCI’s annual conference in May 2019, more than a third of the audience of asset managers and pension funds said they expected to see global assets “operating on ESG principles” move to over 50% by 2024, compared to 25% last year. A May 2019 Harvard Business Review article reported on interviews “with 70 senior executives at 43 global institutional investing firms, including the world’s three biggest asset managers (BlackRock, Vanguard, and State Street) and giant asset owners such as the California Public Employees’ Retirement System (CalPERS), the California State Teachers’ Retirement System (CalSTRS), and the government pension funds of Japan, Sweden, and the Netherlands. We know of no other research effort that involved so many senior leaders at so many of the largest investment firms. We found that ESG was almost universally top of mind for these executives.”

Demand for ESG analytics tools (such as Beyond Ratings) has grown commensurately. Impact investors face even more rigorous and complex measurement challenges. Meeting these challenges prepares all investors for the shape of things to come.

It is good business. The “impact-at-scale” market hasn’t been around long enough to have put up performance numbers. But looking at ESG performance might hold some clues.

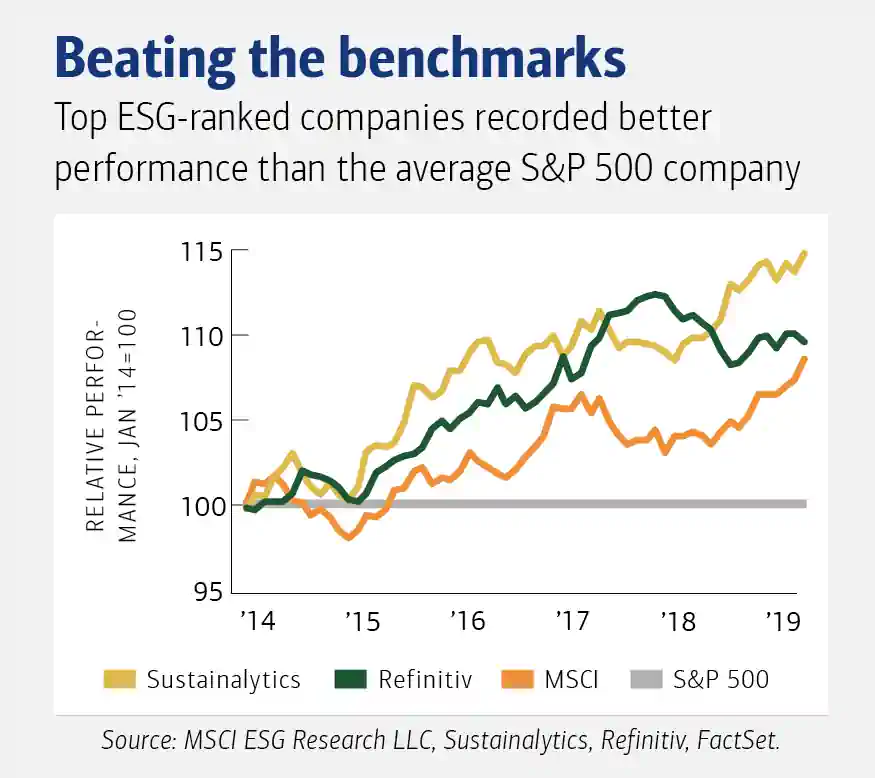

A January 2019 Bank of America report placed members of the S&P 500 into quintiles, according to their ESG rankings. Different data providers don’t always agree on the ratings of any given firm, so the research team ran the analysis using data from Refinitiv, Sustainalytics, and from MSCI (see chart). The pattern from each was clear: “those that scored in the top fifth of ESG rankings outperformed their counterparts in the bottom fifth by at least three percentage points every year for the past five years.” What drove this outperformance? ESG measures tend to be more powerful predictors of future earnings than other metrics such as debt levels. And good ESG ratings lower the risks of costly ESG “blunders.”

Good ESG practices generate their own ecosystem of demand for impact-oriented companies. The list of impact themes is long, and includes monitoring and analytics tools to reduce power and water consumption in various industrial settings (to boost Environmental scores), anti-bias software (increases the pipeline of female and minority executives, for improved Governance scores) low-cost digital education solutions for large workforces (improves Social scores). And again, research focused on just one of these dimensions points to the financial value of getting it right: recent, and very detailed, work by S&P found that firms with female CFOs outperform the broader market.

Frictions matter. In the high-information world of public markets (especially large cap public markets), it is hard to argue that capital will not find opportunities that make a market-rate of return. But the private markets are different. Inefficiencies abound, as Brest and Born noted in 2013. And here, it is true that social and environmental outcomes are achieved that would not have come about but for the capital seeking an impact opportunity.

In sum, there is room in the capital markets for money that seeks a market-rate return and positive environmental and social outcomes. Now that ESG considerations have become mainstream, the pipeline for these opportunities is only set to grow.